David Beckworth argues that the U.S. Federal Reserve should stop running a floor system and adopt a corridor system, say like the one that the Bank of Canada currently runs. In this post I'll argue that the Bank of Canada (and other central banks) should drop their corridors in favour of a floor—not the sort of messy floor that the Fed operates mind you, but a nice clean floor.

Floors and corridors are two different ways that a central banker can provide central banking services. Central banking is confusing, so to illustrate the two systems and how I get to my preference for a floor, let's start way back at the beginning.

Banks have historically banded together to form associations, or clearinghouses, a convenient place for bankers to make payments among each other over the course of the business day. To facilitate these payments, clearinghouses have often issued short-term deposits to their members. A deposit provides clearinghouse services. Keeping a small buffer stock of clearinghouse deposits can be useful to a banker in case they need to make unexpected payments to other banks.

Governments and central banks have pretty much monopolized the clearinghouse function. So when a Canadian bank wants to increase its buffer of clearinghouse balances, it has no choice but to select the Bank of Canada's clearing product for that purpose. Monopolization hasn't only occurred in Canada of course, almost every government has taken over their nation's clearinghouse.

One of the closest substitutes to Bank of Canada (BoC) deposits are government t-bills or overnight repo. While neither of these investment products is useful for making clearinghouse payments, they are otherwise identical to BoC deposits in that they are risk-free short-term assets. As long as these competing instruments yield the same interest rate as BoC deposits, a banker needn't worry about trading off yield for clearinghouse services. She can deposit whatever quantity of funds at the Bank of Canada that she deems necessary to prepare for the next day's clearinghouse payments without losing out on a better risk-free interest rate elsewhere.

But what if these interest rates differ? If t-bills and repo promise to pay 3%, but a Bank of Canada deposit pays an inferior interest rate of 2.5%, then our banker's buffer stock of Bank of Canada deposits is held at the expense of a higher interest elsewhere. In response, she will try to reduce her buffer of deposits as much as possible, say by reallocating bank resources and talent to the task of figuring out how to better time the bank's outgoing payments. If more attention is paid to planning out payments ahead of time, then the bank can skimp on holdings of 2.5%-yielding deposits while increasing its exposure to 3% t-bills.

Why might BoC deposits and t-bills offer different interest rates? We know that any differential between them can't be due to credit risk—both instruments are issued by the government. Now certainly BoC deposits provide valuable clearinghouse services while t-bills don't. And if those services are costly for the Bank of Canada to produce, then the BoC will try to recapture some of its clearinghouse expenses. This means restricting the quantity of deposits to those banks that are willing to pay a sufficiently high fee for clearing services. Or put differently, it means the BoC will only provide deposits to banks that are willing to accept an interest rate that is 0.5% less than the 3% offered on t-bills.

But what if the central bank's true cost of providing additional clearinghouse services is close to zero? If so, the Bank of Canada should avoid any restriction on the supply of deposits. It should provide each bank with whatever amount of deposits it requires without charging a fee. With bankers' demand for clearing services completely sated, the differential between BoC deposits and t-bills will disappear, both trading at 2.5%.

There is good reason to believe that the cost of providing additional clearinghouse services is close to zero. It is no more costly for a central bank to issue a new digital clearinghouse certificate than it is for a Treasury secretary or finance minister to issue a new t-bill. In both cases, all it takes is a few button clicks.

Let's assume that the cost of providing clearinghouses is zero. If the Bank of Canada chooses to constrain the supply of deposits to the highest bidders, it is forcing banks to overpay for a set of clearinghouse services which should otherwise be provided for free. In which case, the time and labour that our banker will need to divert to figuring out how to skimp on BoC deposit holdings constitutes a misallocation of her bank's resources. If the Bank of Canada provided deposits at their true cost of zero, then her employees' time could be put to a much better use.

As members of the public, we might not care if bankers get shafted. But if our banker has diverted workers from developing helpful new technologies or providing customer service to dealing with the artificially-created problem of skimping on deposits, then the public directly suffers. Any difference between the interest rate on Bank of Canada deposits and competing assets like t-bills results in a loss to our collective welfare.

-----

Which finally gets us to floors and corridors. In brief, a corridor system is one in which the central bank rations the number of clearinghouse deposits so that they aren't free. In a floor system, unlimited deposits are provided at a price of zero.

When a central bank is running a corridor system, as most of them do, the rate on competing assets like t-bills lies above the interest rate on central bank deposits. Economists describe these systems as corridors because the interest rate at which the central bank lends deposits lies above the interest rate on competing safe assets like t-bills and repo, and with the deposit rate lying at the bottom, a channel or corridor of sorts is formed.

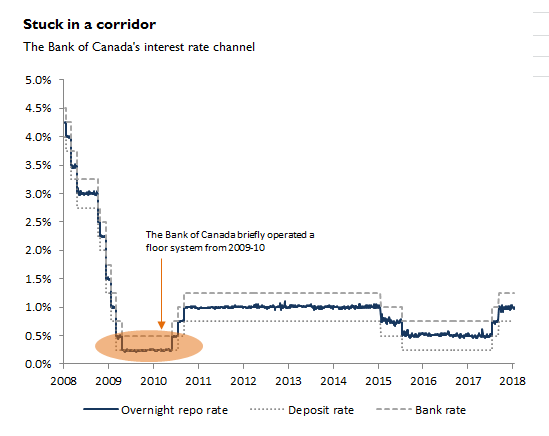

For instance, take the Bank of Canada's corridor, illustrated in the chart below. The BoC lets commercial banks keep funds overnight and earn the "deposit rate" of 0.75%. The overnight rate on competing opportunities—very short-term t-bills and repo—is 1%. The top of the corridor, the bank rate, lies at 1.25%. So the overnight rate snakes through a corridor set by the Bank of Canada's deposit rate at the bottom and the bank rate at the top. (The exception being a short period of time in 2009 and 2010 when it ran a

Let's assume (as we did earlier) that the BoC's cost of providing additional clearinghouse services is basically zero. Given the way the system is set up now, there is a 0.25% rate differential (1%-0.75%) between the deposit rate and the rate on competing asset, specifically overnight repo. This means that the Bank of Canada has capped the quantity of deposits, forcing bankers to pay a fee to obtain clearing services rather than supplying unlimited deposits for free. This in turn means that Canadian bankers are forced to use up time and energy on a wasteful effort to skimp on BoC deposit holdings. All Canadians suffer from this waste.

It might be better for the Bank of Canada (and any other nation that also uses a corridor system) to adopt what is referred to as a floor system. Under a floor system, rates would be equal such that the rate on t-bills and repo lies on the deposit rate floor of 0.75%--that's why economists call it a floor system. The Bank of Canada could do this by removing its artificial limit on the quantity of deposits it issues to commercial banks. Banks would no longer allocate scarce time and labour to the task of skirting the high cost of BoC deposits, devoting these resources to coming up with new and superior banking products. In theory at least, all Canadians would be made a little better off. All the Bank of Canada would have to do is click its 'create new clearinghouse deposits' button a few times.

-----

The line of thought I'm invoking in this post is a version of an idea that economists refer to as the optimum quantity of money, or the Friedman rule, first described by Milton Friedman back in the 1960s. Given that a central bank's cost of issuing additional units of money is zero, Friedman thought that any interest rate differential between a monetary asset and an otherwise identical non-monetary asset represents a loss to society. This loss comes in the form of people wasting resources (or incurring shoe leather costs) trying to avoid the monetary asset as much as possible. To be consistent with the zero cost of creating new monetary assets, the rates on the two assets should be equalized. The public could then hold whatever amount of the monetary asset they saw fit, so-called shoe leather costs falling to zero.

In my post, I've applied the Friedman rule to one type of monetary asset: central bank deposits. But it can also be applied to banknotes issued by the central bank. After all, banknotes yield just 0% whereas a t-bill or a risk-free deposit offers a positive interest rates. To avoid holding large amounts of barren cash, people engage in wasteful behaviour like regularly visiting ATMs.

There are several ways to implement the Friedman rule for banknotes. One of the neatest ways would be to run a periodic lottery that rewards a few banknote serial numbers with big winnings, the size of the pot being large enough that the expected return on each banknote as made equivalent to interest rate on deposits. This idea was proposed by Charles Goodhart and Hugh McCulloch separately in 1986.

Robert Lucas once wrote that implementing the Friedman rule was “one of the few legitimate ‘free lunches’ economics has discovered in 200 years of trying.” The odd thing is that almost no central banks have tried to adopt it. On the cash side of things, none of them offer a serial number lottery or any of the other solutions for shrinking the rate differential between banknotes and deposits, say like Miles Kimball's more exotic crawling peg solution. And on the deposit side, floor systems are incredibly rare. The go-to choice among central banks is generally a Friedman-defying corridor system.

One reason behind central bankers' hesitation to implement the Friedman rule is that it would threaten their pot of "fuck you money", a concept I described here. Thanks to the large interest rate gaps between cash and t-bills, and the smaller gap between central bank clearinghouse deposits and t-bills, central banks tend to make large profits. They submit much of their winnings to their political masters. In exchange, the executive branch grants central bankers a significant degree of independence... which they use to geek out on macroeconomics. Because they like to engage in wonkery and believe that it makes the world a better place, central bankers may be hesitant to implement the Friedman rule lest it threaten their flows of fuck you money, and their sacred independence.

That may explain why floors are rare. However, they aren't without precedent. To begin with, there is the Fed's floor that Beckworth describes, which it bungled into by accident. At the outset of this post I called it a messy floor, because it leaks (George Selgin and Stephen Williamson have gone into this). The sort of floor that should be emulated isn't the Fed's messy one, but the relatively clean floor that the Reserve Bank of New Zealand operated in 2007 and Canada did from 2009-11 (see chart above). Though these floors were quickly dropped, I don't see why the couldn't (and shouldn't) be re-implemented. As Lucas says, its a free lunch.

I always assume the much simpler corridor.

ReplyDeleteThe central banks declares it will carry at most a quarter point of fiat at risk, fiat it may lose or gain permanently.

Deposits have to cover loans for the rest,and interest charges applied when the fiat at risk exceeds a quarter point. Transaction costs are zero, that is fine.

The central bank will occupy whatever part of the short end needed to make this happen.

In your construction, you removed all the roundabouts. Simply ask what is the shortest currency issuance path. The currency issuer is a market maker, matching loan to deposits and will carry a market making risk of some bounds. Thus, the best information available to the currency issuer is the current distributions of loan and distribution of deposits and then outstanding currency risk (matching error carrier on the books). The risk bpundsbeing the corridor.

DeleteJust assume market matching function is optimum, thus the interest flow, from loans to deposits, can be set such that market making error is minimum. All parties know the rule, all parties have equal view of the loans to deposit distributions, all parties can drop asynchronous bid and ask.

Then insurance companies can look at the matching error over time and create an interest rate which must be insured, as it is a nominal value, an estimation after the fact.

Dunno Matt, not sure if you got my post. Probably my fault. Try summarizing my post in one paragraph using your own words and I'll tell you how close you are, and then once we're on the same page why don't you go ahead with your criticisms.

DeleteGood post.

ReplyDeleteTypo: " (The exception being a short period of time in 2009 and 2010 when it ran a corridor)." should be floor.

Thanks Nick, fixed.

DeleteJ.P., your article entirely overlooks the difference between a system that merely adheres to the Friedman rule (which is actually a rate below that on government bonds, which are term rather than overnight instruments) and one that pays an above-Friedman-rule return on CB deposits, as the Fed has done ever since November 2008, and as any floor system is likely to do in practice, since you can keep such a system going with an overly-high IOER rate, but not with one that errs the other way.

ReplyDeleteIn fact the true Friedman rule rate, allowing for transactions costs, is much lower than the rate on Treasuries. On this see: http://onlinelibrary.wiley.com/doi/10.1111/jmcb.12394/full).

More generally getting banks to pile-on excess reserves is not "economical," as you claim, for reasons I pointed out in replying to similar claims made on a Liberty Street post (https://www.alt-m.org/2017/10/03/strange-official-economics-of-interest-on-excess-reserves/).

But my main concern with your post is that is seems to completely neglect the monetary control implications of a floor system. Such a system is, in essence, nothing other than a purpose-made, above-zero permanent liquidity trap. As such it suffers all the unfortunate monetary control shortcomings of any liquidity trap. The standard monetary transmission mechanism simply doesn't function because reserves cease to have an opportunity cost, at least relative to all longer-maturity assets. As for the alternative "portfolio effect" transmission mechanism on which Bernanke & Co. set their hopes starting in 2009, we have seen just how weak that mechanism is: under it, trillions of dollars in asset purchases accomplished less than billions might be expected to have accomplished under a traditional framework. It is for this reason that I fear we may one day find ourselves referring to Jerome Powell as "The Six Trillion Dollar Man.)

For the last several years, Canada's core CPI inflation rate has been almost spot-on the Bank of Canada's 2% target; whereas in the U.S. the PCE and core CPI inflation rates have remained persistently below 2% since that target was introduced at the start of 2012. (Intriguingly, it was also during that brief interval during which Canada implemented a floor system that Canada experienced an extraordinary bout of headline CPI _deflation_!) All this is quite in accord with floor systems' built-in deflationary bias, to which I've also drawn attention (https://www.alt-m.org/2017/09/19/the-two-per-cent-solution/).

In short, the last thing Canada needs is to follow our (US) bad example. Generally speaking, it has resisted that temptation. I for one hope it keeps resisting it!

In my sentence "at least relative to all longer maturity assets," "all" should be "many"!

DeleteHi George, thanks for stopping by.

Delete"...and as any floor system is likely to do in practice, since you can keep such a system going with an overly-high IOER rate, but not with one that errs the other way."

Correct me if I'm wrong, but you seem to be saying that all floor systems are characterized by an overnight rate that trades below the floor rate. But eyeballing the above chart of BoC interest rate policy, the overnight repo rate stayed very close to the deposit rate when it ran a floor system back in 2009-10.

"The standard monetary transmission mechanism simply doesn't function because reserves cease to have an opportunity cost, at least relative to all longer-maturity assets."

I don't understand why the standard monetary transmission mechanism ceases to function when we are in a liquidity trap. BoC deposits are still the unit of account. And by reducing the deposit rate, the central bank can set off the good ol' hot potato effect. And it sets off a reverse hot-potato effect when it increases the deposit rate. The names and tools are a bit different, but this is still regular monetary policy.

"In fact the true Friedman rule rate, allowing for transactions costs, is much lower than the rate on Treasuries. On this see: http://onlinelibrary.wiley.com/doi/10.1111/jmcb.12394/full). "

Thanks. Will have to read it.

Ungated version is here, for anyone who is curious:

http://faculty.georgetown.edu/canzonem/OIR_paper.pdf

"Correct me if I'm wrong, but you seem to be saying that all floor systems are characterized by an overnight rate that trades below the floor rate." Not so, JP: none of my criticisms have to do with the "leakiness" of the US system. I regard that leakiness as a minor side-show. It only means that there is still some fed funds activity, mainly between GSE's and banks, at rates below IOER rate.

DeleteThe standard monetary transmission mechanism cannot function once reserves have no opportunity cost. In that case, open-market purchases translate into like increases in bank excess reserve holdings, rather than into like increases in bank lending/asset purchases. The money stock does not increase, or increases very little. The traditional transmission mechanism depends on the capacity of central bank reserve creation to spur money growth.

This is all very orthodox--no crazy Selgin heresies are involved! It is indeed one reason why policymakers worried about a "zero lower bound" problem.

As for the "hot potato effect," it is attenuated in a floor system unless the deposit rate is reduced to the point where one reverts to a corridor! The statement: "The opportunity cost of reserve holding is zero" and the statement "excess reserves are no longer a hot potato" mean the same thing.

Ok, I'm confused about your last paragraph. But let me setup an example to see where we differ.

DeleteLet's say it's 2009 and the BoC is running a floor system at 0.25%. The BoC issued $3 billion in settlement balances to implement its floor whereas subsequent research showed that only $1.5 billion or so was actually necessary to drive the overnight rate down to the deposit rate.

The BoC wants to loosen monetary policy. We both agree that open markets purchases have no effect, because the demand for settlement balances has long since been sated.

Even though open market operations have been neutered, the BoC can still loosen policy by reducing the deposit rate to 0%. BoC deposits suddenly provide banks with a sub-market return. A hot potato effect is set off as banks try to offload BoC deposits and buy higher yielding assets, including (but not limited to) t-bills and other short term debt that continue to yield 0.25%. This process ends with the yields on these short term instruments once again falling to the floor, which now lies at 0%.

Is there anything wrong with that story? Your comment at 4:01 PM could be read as a criticism of my last paragraph, but I could be wrong.

"The BoC issued $3 billion in settlement balances to implement its floor whereas subsequent research showed that only $1.5 billion or so was actually necessary to drive the overnight rate down to the deposit rate." Central bank asset purchases cannot themselves drive real rates permanently below their "natural" levels. (They tend on the other hand to raise nominal rates in the long run.) Establishing a floor system is a matter, not merely or fundamentally of creating a large nominal stock of reserves, but of setting the real CB deposit rate high enough to eliminate the opportunity cost of reserve holding, which (in the long run) means setting it above natural rates on short-term non-reserve assets.

DeleteThis means that it is NOT generally possible, within the confines of a proper floor system, for the CB to lower the deposit rate however much it needs to to achieve a particular nominal target. In your example, for instance, while a zero deposit rate might be what's called for to achieve that end, such a rate is also (in your example) below the rate required to maintain a floor system. Instead, it results in a switch back to a corridor system (as would any move to a positive deposit rate that is nonetheless low enough to discourage banks from holding more than minimal reserve balances). This is the point of my previous comment's last paragraph: reserves are never a "hot potato" in a floor system.

In short, a floor system may in some (indeed, many) situations allow for adequate monetary easing only in the sense that the CB retains the option of abandoning it, which is what your example actually has it doing.

"The basic idea behind this [floor system] approach is to remove the opportunity cost to commercial banks of holding reserve balances by paying interest on these balances at the prevailing target rate." See Keister et al., "Divorcing Money from Monetary Policy" (the title says it all!), https://www.newyorkfed.org/medialibrary/media/research/epr/08v14n2/0809keis.pdf

Delete"In your example, for instance, while a zero deposit rate might be what's called for to achieve that end, such a rate is also (in your example) below the rate required to maintain a floor system. Instead, it results in a switch back to a corridor system (as would any move to a positive deposit rate that is nonetheless low enough to discourage banks from holding more than minimal reserve balances). "

DeleteLet's hone in on where you specifically disagree with my example. I hypothesized that if the 2009-era BoC had cut its deposit rate to 0% from 0.25%, then the repo rate would follow to 0%. (Remember, the BoC had gone overboard in sating the demand for settlement balances, issuing $3 billion when far less was required to set a floor at 0.25%.) Are you saying that in the event of a cut to 0%, the Canadian repo rate would have stayed at 0.25%?

I cannot speak with special authority on the Canadian case; but (1) I am pretty certain that the BofC should in fact have dropped its deposit rate to 0 in 2009-10; and (2) I am not convinced that the repo rate would in turn have dropped all the way to zero. It might well have fallen less, in which case Canada would have found itself back in a corridor. And if it didn't, that would be a reason for supposing that the deposit rate was still too high, that is, that what was really needed was a negative rate (as many believed at the time). It is hard to come up with a scenario in which the rate that keeps the floor system in place is also not an overtight rate. That's because the rate must be such as will make reserves more attractive than other assets, which means one that puts the breaks on broad money growth. One may in turn issue all the base money one likes. But it just piles up--that is, the reserve multiplier just falls passively to an offsetting degree.

Deletehe reason I say that Canada should not have held its overnight rate at 25 basis points starting in 2009:Q1 is that it was at that time that Canadian nominal GDP growth, which has previously hovered around an already meager 2%, plunged to _minus_ 4%, and did not recover its lost ground until the end of the year. The Canadian authorities, following the bad example of their US counterparts, were so afraid of having their rate target hit the dreaded "zero lower bound" that they created an above-zero liquidity trap. As I have written elsewhere, this strategy is like building a wide veranda around the first floor of a skyscraper, to keep anyone who jumps from the top of it from ever hitting the ground.

DeleteGeorge, I must confess that after all our back and forth I still don't understand your point.

DeleteIn my BoC example, the Bank starts with a floor at 0.25% and then loosens by reducing the deposit rate to 0%, at which point the overnight follows to 0%. We'll assume that the $3.0 billion in settlement balances that the BoC has used to set up its 0.25% floor is sufficient such that the ratcheting down of the deposit rate leads to a clean fall in the overnight rate to 0%.

Alternatively, if the BoC is running a channel system, with the deposit rate at 0% and the overnight rate at 0.25%, then it can conduct traditional open market purchases and drive the overnight rate to 0% (the deposit rate falling to 0.25%).

Now correct me if I'm wrong, but you seem to be saying that traditional open market operations conducted in a corridor system are a better method for doing monetary policy. But given that the overnight rate ends up at 0% in both scenarios, it seems to me that the floor and corridor systems do the exact same thing. In other words, the "hot potato effect" is not attenuated in the BoC's floor system. Both systems are capable of setting off a daisy chain of banks desperate to rid themselves of excess settlement balances, with the decline in the overnight rate to 0% in each scenario being proof.

But I could be entirely misunderstanding your point.

"(the deposit rate falling to 0.25%)."

DeleteCorrection. To -0.25%.

JP, you say, "Both systems are capable of setting off a daisy chain of banks desperate to rid themselves of excess settlement balances." But it is the very essence of a floor system that the deposit rate must be such as to eliminate the opportunity cost of reserve hoarding, so that banks lack the incentive to minimize their reserve holdings that would otherwise make excess reserves a "hot potato." It is only when the deposit rate falls below the overnight rate that the "hot potato" effect again takes hold. But in that case the floor system has in fact been abandoned. You seem to assume that the overnight rate must follow the deposit rate wherever the latter goes, but that isn't correct. A sufficiently low deposit rate will at some point diverge from the overnight rate. That doesn't happen going up, for any deposit rate equal to or above the "natural" overnight rate rules the roost. Visually, have a look at the fed funds market supply demand schedule from Goodfriend in my "@ percent solution." For a given reserve stock, as you lower the IOER rate, eventually you come to a point where you are on the sloping part of the funds demand schedule. At that point, excess reserves again become a hot potato, the multiplier revives, but you are no longer in a floor system. On the other hand, the IOER rate can be raised without limit, cet par., without undoing the floor or reviving the multiplier.

Delete"@ percent solution." Sorry: that should be "2 Percent Solution." Here's the URL:

Deletehttps://www.alt-m.org/2017/09/19/the-two-per-cent-solution/

George, I want to stick to the specific example of the BoC's 0.25% floor that I've been using so we can nail down exactly where we differ. In my comment at 9:37AM, I claimed that in both scenarios the exact same monetary policy goal is achieved because they both end up with the Canadian overnight rate falling from 0.25% to 0%. It seems to me like you disagree with that, but maybe you don't?

DeleteIt is not necessarily the case that the overnight rate will follow the deposit rate to any arbitrarily-specified level. That depends on circumstances. That's the point of the chart to which I refer above. If the natural equilibrium market rates are above zero, the overnight rate will not follow the deposit rate all the way to zero; and it is ONLY in that case that reserves become a "hot potato." So, you can have your floor system, or your hot potato, but not both. That is the point.

DeleteYou seem to think instead that under a floor system the deposit rate always determines the overnight rate, no matter how low the floor is set. But if the deposit rate declines sufficiently, it will fall below market rates, reviving the multiplier, which will ultimately re-establish a corridor system with scarce reserves and overnight>deposit rate. The Friedman Rule assumes, remember, a given or exogenous real market rate. So one can't stick to it (and implied zero opportunity cost of reserves) and yet have the deposit rate fall to any level one posits.

George, you keep avoiding my specific example. And I'm begging you to at least speak to it because otherwise I can't figure out where we differ. One of my deficiencies is that I only learn through actual examples.

DeleteSo the assumption from my comment on Jan 17, 2018 at 9:37 AM was that the $3.0 billion in settlement balances that the BoC has used to set up its 0.25% floor was sufficient such that a ratcheting down of the deposit rate to 0% would lead to a clean fall in the overnight rate to 0%. Which means there is no difference between a BoC 0.25% floor system and a BoC corridor with the overnight rate at 0.25%. Because they both end up with the Canadian overnight rate falling from 0.25% to 0%, the exact same monetary policy goal is achieved.

I still don't know if you agree with that or not. Once I know then we can move on.

I don't agree, JP--that is, it may not be possible for the BofC to permanently drive the overnight rate to 0 by lowering its deposit rate to zero. In your example, you say that initially the 0 deposit rate is "sub-market," and that this means banks try to dispose of their surplus reserve balances, putting downward pressure on the overnight rate, and perhaps on some other rates. So far, so good. But in order for the long-run equilibrium to consist of the overnight rate and other market rates adjusting to conform with the new (0) deposit rate, that deposit rate has to be consistent with natural rates. If it is below, rising aggregate demand will eventually cause credit demand to rise, offsetting the outward supply shifts. This is just Wicksell's story of short run vs. long-run effects of expansionary policy. In that case, instead of establishing a new "floor" with overnight = deposit = 0, the BofC ends up switching to a corridor with overnight rate above deposit rate lower bound, and (if 0.25 was itself "natural" rate) perhaps no long-run change in overnight market rate at all.

DeleteNote that, if BofC moves to 0 in sympathy with drop in natural rates from .25 to 0, then the move will go through as you suggest. But note that if bank is too concerned to keep floor system in place, it may be inclined to err on side of over-tightening, which though itself undesirable does not result in switch to corridor.

"...it may not be possible for the BofC to permanently drive the overnight rate to 0 by lowering its deposit rate to zero. In your example."

DeleteBut in the instant after the drop in the BoC's deposit rate to 0%, the overnight will rapidly follow to 0%. Right? Again, this is given my assumptions from January 18, 2018 @ 11:48 AM. And in those few instants, the BoC's floor system has provided the same sort of monetary stimulus that a corridor system would provide when open market operations drive the Canadian overnight rate from 0.25% to 0%.

The overnight might drop to 0 for a while, JP. But I must caution you that most analyses of floor systems do not ever imagine the temporary deviation from the floor your story entails, with its setting of a "sub-market" deposit rate. They assume that the deposit rate, even when reduced for the sake of easing the CB policy stance, remains continually at or above the market rates, so that reserves continue to have a zero opportunity cost (or, put another way, the Friedman rule, as they understand it, is always adhered to). The floor system monetary transmission mechanism works via a "portfolio" effect rather than by means of the conventional multiplier/hot potato mechanism to which your account refers. So you are telling a monetary easing story that is not fully consistent with the workings of an orthodox floor arrangement. It is instead a story in which the floor is at least temporarily abandoned. Moreover, for the reason I explained previously, it will also tend to involve a permanent abandonment of the floor is the new (0) deposit rate is not just "sub-market" but "sub-natural."

DeleteForgive me for interrupting, but the last two comments are a clean illustration of the erroneous causalities embedded in orthodox monetarism.

DeleteThe stimulus that JP is referring to directly in his entire sequence of comments is the stimulus from a policy rate decline – NOT the stimulus from any particular bank reserve effect (correct me if I’m wrong JP). I agree with JP’s rate analysis throughout these comments.

By contrast, the legitimacy of the entire monetarist story of stimulus according to excess reserves is one of the core, underlying issues here. This story is fundamentally wrong according to some opinions (including mine) – i.e. the entire multiplier causality story is wrong. We’ve been over that many times.

But the other thing that is fundamentally wrong here – again in my opinion – is this idea that short dated market rates somehow exist independently of Fed policy in its targeting of funds rates and/or IOER. This is backwards. It is Fed policy from which the market takes its cue in order to determine the constellation of short date interest rates – with all the noise and spread imperfection that is involved in GSE arbitrage, repo activity, Treasury bill liquidity, etc. That’s the anchor. The market then extrapolates that to the longer dated term structure across the full credit spectrum, taking into account expectations for Fed policy and even “natural rate” type assumptions about rates “should” be headed or where they “belong” as reflected in the existing term structure. But the causality of - Fed to market - rate determination at short dates is how it actually works – not the reverse. It is a fundamental error to suggest that the Fed somehow sets its short dated (i.e. overnight for the most part) policy rate structure “less than” or “greater than” “natural” market rates. The Fed is the anchor for short term market rates. And the reason for this is that the banks in the US and Canada and other modern economies are simply too big not to determine the arbitrage causality as flowing from the central bank rate - to commercial bank action - to general market rates. The reverse error seems to be another fundamental mistake of monetarism in this area of analysis, because it is ignoring institutional proportions. Finally, it’s not 1923 anymore. The suggestion that commercial banks somehow assume a mission of converting several trillion in excess reserves to required reserves requires a scenarios of astronomical balance sheet expansion that is simply too absurd to even consider in a modern banking system.

" Finally, it’s not 1923 anymore. The suggestion that commercial banks somehow assume a mission of converting several trillion in excess reserves to required reserves requires a scenarios of astronomical balance sheet expansion that is simply too absurd to even consider in a modern banking system." It is, in fact, 1923 still in all places where vast reserve expansion is not offset by high reserve deposit rates. Look at any recent hyperinflation if you doubt this.

DeleteAs for the Fed ruling the interest rate roost, that is the superficial view. The relatively sophisticated one is still Wicksell's. ca. 1898. Sometimes, newer isn't better. The Fed's post-2008 IOER rate adjustments have been made in response to prior upward movements in market rates, not the other way around. If you don't believe it, eyeball this chart: https://fred.stlouisfed.org/graph/fredgraph.png?g=hCLO

Yes - but there's term structure in those comparisons, an effect which I noted in my comment above. That doesn't disprove the Fed as the origin of causality in spread outcomes across the same term - i.e. overnight.

DeleteI also don't think episodes where the market correctly forecasts future Fed moves through term structure means that the Fed "follows" the market in all cases. This just isn't so, even if the market's forecasts turn out to be correct. I think the converse is demonstrated logically by the market's dynamic rate response out the term structure to Fed rate announcements that are not preceded by near certainty of expectation. Anything that is not absolutely certain is in some sense a surprise, instilling a further market reaction.

The Fed can resist anything - provided it is prepared to live with all peripheral consequences such as an exchange rate effects, etc. But those are issues that are separate from that of identifying the true origin of causality in respect of actual policy rates and the comparable short term market rate structure.

As I said above, I think the causality flows from the Fed to the market across the overnight term structure. That's where the actual Fed action is - normally. The game from there in the context of term structure and future actual Fed action is one of interacting expectations and confirmation or not of expectations - via term structure.

Referring to above chart, you will see that increases in Treasury rates, and in the longer-term rates especially (which are most independent of Fed policy rate) anticipate IOER increases, typically by more than a month. Yes, markets may be anticipating the Fed; but it is far from evident that the Fed is not anticipating market tendencies, as it is indeed expected to do.

DeleteFor sure - its a game where each anticipates the tendencies of the other. But that can compound like Keynes' beauty contest.

DeleteAnd the Fed always has a choice about whether, when, and how much to change its policy rate. The market will then respond to that actual choice.

And I've seen too much in olden days Bank of Canada to know that mighty CB resistance and victory over market interest rate expectations is very possible.

It's not inconceivable I could adjust my thinking about this.

DeleteBut this part intersects with the multiplier causality part - where it is absolutely certain I could not adjust my thinking.

George, you said:

Delete"The overnight might drop to 0 for a while,"

Well, at least we seem to sorta agree on that point. The overnight rate drops to 0% *in the next instant*, just as it would if the BoC did open market operations in a corridor. You qualify it with the word *might*--which I think is wrong. It *must* fall to 0% given the assumption I've provided. But in any case, given that we sort of agree that it falls to 0%, then we should be able to agree that *in that instant*, a corridor and floor system provide the exact same monetary stimulus to the economy.

JKH, you said:

"But the other thing that is fundamentally wrong here – again in my opinion – is this idea that short dated market rates somehow exist independently of Fed policy in its targeting of funds rates and/or IOER. This is backwards. It is Fed policy from which the market takes its cue..."

I agree. If a central bank wants the overnight rate to be x%, then the overnight rate will be x%, whether it is running a floor or a corridor.

"I agree. If a central bank wants the overnight rate to be x%, then the overnight rate will be x%, whether it is running a floor or a corridor." But this was manifestly not the Fed's experience during the last months of 2008, when the overnight (fed funds) rate fell increasingly further below its target. I refer here not just to the "leaky" floor system but to what happened in the weeks prior to the implementation of IOER. On October 2, for example, the effective ffr dropped to .67% while the target rate was still 2%.

DeleteI think some semantics here need clarifying. A central bank cannot have any short-term rate that it wants AND meet any inflation target it sets, because there is a real short term natural rate, as there are other natural rates, that lie beyond its control. This is why the Fed, to stick for that examples, readily ponders r*, and why it worries about getting its future value wrong. Central banks must at least implicitly take exogenous r* (real natural rate) changes into account in setting their policy rates. Otherwise their rate settings will not prove sustainable given their ultimate objectives, or merely given their desire to avoid triggering a cumulative process. Back in the early 1980s, the ffr target briefly exceeded 20 percent. Could the Fed have kept it at 2% had it so wished? Not unless it wanted to see inflation spiral out of control. This is the old Wicksell story. The only point is that overnight rates are not exempt. Indeed, the Wicksell story was always, fundamentally, about the consequences of trying to peg the wrong policy (i.e., short-term or overnight)rate.

Delete“Central banks must at least implicitly take exogenous r* (real natural rate) changes into account in setting their policy rates.”

DeleteThat sentence and the full paragraph of your comment are quite understandable. The Wicksell cumulative process and your 1980’s counterfactual are very intuitive and realistic. And while I’m not an academic, it seems to me that the r* idea could allow a fair bit of philosophical debate about what it really means or could be allowed to mean relative to policy and market actions around r.

But again, you seem to be referring to a rate path as reflected in the term structure of rates and the inevitable groping of policy rates along that path, with the inevitable corrections that will occur in revised expectations and in the term structure. And this seems to be a very different issue than how the overnight term structure of the full constellation of different rate types will align itself to a particular actual Fed policy target, and how that gets reflected in the relationships of the target policy rate, IOER, or corridor bound rates.

(The 1980’s was my time of action. There were many cases in which the Fed and the Bank of Canada would make massive injections or massive withdrawals of reserves in order to cause that entire overnight rate structure to respond in the most dramatic way in both directions as rates made their upward move to a 23 per cent bank prime rate in Canada and somewhat less I think in the US. And the term structure of market rates would respond to this policy volatility as well – in almost equally violent fashion in some cases. This market action all originated with very specific CB reserve setting changes and corresponding commercial bank behavior, spreading out to the rest of the community. Yes - the CBs and the commercial banks ruled the roost in terms of the epicenter of it all and its effect.)

Perhaps a cynic’s view of the natural rate idea is that CB’s can’t opt out of the actual future path of their own policy actions. Whether they are steered at the time by the natural rate, God, foreign exchange responses, or what they ate for breakfast doesn’t seem to matter in that way.

DeleteI'm actually not that cynical, but I remain to be persuaded on the idea.

"But this was manifestly not the Fed's experience during the last months of 2008, when the overnight (fed funds) rate fell increasingly further below its target."

DeleteJust because it can always hit its rate target doesn't mean it will always choose to hit it.

"I think some semantics here need clarifying. A central bank cannot have any short-term rate that it wants AND meet any inflation target it sets, because there is a real short term natural rate, as there are other natural rates, that lie beyond its control."

Yep, you won't get any debate from me on that.

Where we seem to differ is on the relative merits of the two mechanisms for setting short term rates at a level consistent with the central bank's inflation target. You say that a floor system suffers from "unfortunate monetary control shortcomings." I say a floor and a corridor have the exact same monetary control properties. In the BoC example we just worked through, it seems we at least agree (sort of) on what sort of conditions might lead the two systems to provide the same degree of monetary stimulus to the economy. After all, in both the corridor and floor the Canadian overnight rate instantaneously fell to 0%.

" But what if these interest rates differ? If t-bills and repo promise to pay 3%, but a Bank of Canada deposit pays an inferior interest rate of 2.5%, "

ReplyDeleteI dont see how the BOC can change that. If it increases the deposit rate the t-bill rate will rise, as the difference is the product of the decisions of participants in the market for t-bills.

The deposit rate influences the lowest interest rate t-bill buyers will bid t bills up to, and influences all longer rate bonds accordingly.

The BoC creates an initial yield differential between the rate on BoC deposits and on repo/t-bills by making BoC deposits incredibly rare, not by altering the deposit rate. By doing so, banks will pay a premium to hold BoC deposits. Put differently, if rare deposits yield 2.5%, then only a 3% rate on plentiful short-term t-bills will balance out banks' preferences between BoC deposits and short-term t-bills. If that rarity is removed by the BoC, then banks' will become indifferent between deposits and t-bills, the rate on t-bills now falling to 2.5%.

Delete"The BoC creates an initial yield differential between the rate on BoC deposits and on repo/t-bills by making BoC deposits incredibly rare, not by altering the deposit rate." In the short run, yes; but in the long-run the demand for BofC deposits depends on the nominal scale of the banking system (or, if you like, the size of the base money multiplier). In the long-run, a floor system requires a real deposit rate at or above the "natural" rate on equivalent (risk-free, overnight or callable) loans.

DeleteThis goes the other way as well. Suppose that the Fed had tried to switch to a floor system, not by moving from a zero to a positive (and above-natural) IOER rate, buit byu simply starting to create oodles of reserves in an effort to make them cease to be scarce. Since excess reserves would still have carried an opportunity cost, banks would have swapped them for other assets, maintaining the established money multiplier by means of an increase in their overall balance sheets proportional to the increased reserve stock. Reserves would thus end up being just as scarce as before, and T bill rates would not permanently decline. In short, monetary neutrality applies.

Getting to a floor system instead requires that the Fed adjust its administered IOER rate upwards enough to eliminate the opportunity cost of reserve holding. So long as banks are paid at least as much (in practice it is usually more) to hold reserves as they can get by swapping them for other interest-earning assets), the equilibrium money multiplier is permanently reduced. Thuis is indeed what happened in the U.S. case: it mattered, in other words, that the above-zero IOER rate went into effect in anticipation of massive reserve creation by the Fed. Otherwise banks would have disposed of excess reserves that came their way. Preventing them from doing so was, moreover, the EXPRESS reason why the Fed asked to be able to pay non-zero IOER in the first place.

I dont see how the BoC can remove the differential, as whatever the deposit supply is, the causality is still from deposits to t-bill . Make deposits less rare and the rate goes down and the effective t bills rates also fall, but the t bills are still higher yield. There is cost of trading in and out and a risk premium as for one thing the t-bill has a fixed coupon, and the deposit does not.

Delete"Make deposits less rare and the rate goes down and the effective t bills rates also fall, but the t bills are still higher yield." Again, the general decline in real rates doesn't usually persist in in the long run, when money expansion pushes up demand schedules across markets, including those for every sort of credit. To suppose otherwise is to toss out standard long-run monetary neutrality propositions. Knut Wicksell wouldn't do so, and I stand with the ol' Swede!

DeleteIf the decline doesn't persist then then the differential persists even more so.

DeleteWhat JP says

ReplyDelete(all of it)

Let me elaborate (quick and dirty).

DeleteThe argument pushing back on JP’s assumptions reflects a misunderstanding of how commercial banks actually manage their reserve positions, “monetary theory” notwithstanding. A floor system with IOR at 1 per cent has essentially the same monetary transmission effect as a corridor system with a target policy rate of 1 per cent. There is no essential difference in terms of how the presumed “opportunity cost” element affects the outcome.

The CB controls rate targeting under a corridor system by fine tuning a relatively scarce quantity of excess reserves. The CB controls rate targeting under a floor system by paying the target rate on a “super-excess” quantity of excess reserves.

The pre-2008 Fed system was an “asymmetric” corridor system in effect, with the rate on deposits being 0, whatever the target rate. The Bank of Canada system is the standard “symmetric” corridor system, with the rate on deposits and the LOR rate framing the target rate symmetrically on either side.

Minor operational/arbitrageable “bugs” may exist. For example, it is well known that certain institutions keeping deposits with the Fed do not earn IOR. But such glitches do not affect the fundamental outcome in the big picture. The Fed could control the target rate at around 2 per cent for example by paying IOR of 2 per cent in a floor system (a system essentially now in place under QE and QE exit) or by targeting 2 per cent under either a symmetric or asymmetric corridor system.

The typical interpretational error relates to knowledge of how banks manage their reserve positions. The floor system generally allows for more excess reserves than the corridor. The question is how banks react to those “super-excess” reserves under the floor versus relatively scarce reserves under the corridor. And the correct answer, unfortunately obscured by conventional economics textbooks for decades, is that there is not a whole lot of difference when compared to a corridor with the same effective policy rate target.

The decision of the central bank to target 2 per cent will result in a full configuration of money market rates that is consistent with a general policy rate level of 2 per cent under either system. The rate spectrum will settle in at about the same configuration under either system - other things equal.

What is typically not appreciated is that banks make their risky lending decisions based on risk assessment, required capital quantity, and required return on capital. This is what determines the required credit spread. This has nothing to do with the availability of reserves. The purpose of excess reserves in particular is to provide the means of interbank settlement of payments. It is not to support increased lending. Banks do not respond to super-excess floor reserves by panicking and desperately buying all the junk bonds they can get – (to make a point) - just to “use up” the excess reserves that the CB has created under a floor system. This is just not how banks behave economically, obviously.

…

…

DeleteBanks lend according to views on credit risk and interest rate risk. They do not make risky credit decisions based on the availability of risk free reserves.

Participating banks under a floor system are smart enough to understand that “hot potato” economics does not “use up” the level of system reserves. Furthermore, it is stunning that an obtuse argument still remains widespread in economics that conspires to attribute bank lending behavior according to the expected migration of “excess reserves” to “required reserves” in order to “use up” excess reserves. First, such migration occurs at a glacial pace relative to the enormous quantity of excess reserves available under QE (for example), due to small fractional ratios for required reserves. Such excess reserve migration nonsense just doubles up on the more fundamental error in misunderstanding lending economics. Moreover, commercial banks understand the self-destructive nature of such “hot potato” recklessness implied by such erroneous interpretations of bank behavior under such a floor system reserve environment. The major US banks totally understand the correct economics in the context of QE, and are certainly not dumb enough to proceed to lend recklessly in the QE environment, simply in an effort to “get rid” of reserves that they may hold on an individual basis.

The actual “hot potato” dynamic in a corridor system is all about ensuring CB success in targeting the policy rate. It's all about setting the interest rate and providing the system with the excess reserves it demands with the objective of maintaining that interest rate on track with target. The “hot potato” works through the effect of money markets on the actual day to day behavior of the rate being targeted. It has nothing to do with “secular” lending behavior. We can understand this in a very obvious way. For a given target rate, there is no reason why the daily probability for a temporary increase in excess reserves should be different than the daily probability for a temporary withdrawal of excess reserves. That's just the way the system works and the way the CB responds to various circumstances in which reserve distribution causes undesirable temporary tightening or easing conditions in money market rates, thereby steering the rate being targeted by policy this way or that way, off course in such a way as to require subsequent correction. The central bank is constantly adjusting the excess reserve setting in order to steer the rate being targeted under a corridor system, and especially under the pre-2008 asymmetric Fed system. Decades of data of daily excess reserve settings can confirm this for pre-2008 Fed system. The hotness of the potato is all about correcting wayward overnight rates under a given target policy rate. It’s not about banks expanding their lending in some fundamental way in order to "use up" excess reserves.

…

…

DeleteThus, the “opportunity cost” under a corridor works by way of correcting wayward funds rates under a given target - and it works in both directions in any given reserve averaging period. Excess reserves are not a “source of funds” for secular loan expansion.

This is precisely where Neanderthal textbooks reflect a stunning ignorance of actual reserve dynamics, preferring a fantasy tale of causality according to a “money multiplier”. This multiplier nonsense is the area that has been debunked in papers put out by the Fed, the Bank of England, and others. And of course it is the area characterized as “endogenous” money creation by banks, as described by various “heterodox” sources. And whatever else one may think of MMT, it is a core fact that is quite correct and central in their own version of heterodox framing.

What this means is that the version of “opportunity cost” under a corridor system is essentially not much more useful than its presumed absence under a floor system. The spectrum of money market rates will settle in to pretty much the same economic spread levels under either system, driven by the discipline of bank capital management rather than erroneous reserve economics.

It is also important to recognize that money market rates react almost instantaneously to changes in CB policy rate targets. The opportunities for speculation or arbitrage are limited in such a way that the expansion of bank money market asset portfolios are similarly limited. Banks only attempt to “use” their reserves under such dynamic change conditions insofar as they expect to make money from their own expectations about interest rates. But endogenous money creation still rules the roost. And the CB will inevitably act to cause reverse direction flows at some point in order to stop out any rate decline in the transition from one target level to the next in a downward rate cycle, for example. And obviously that whole dynamic works in reverse when target rates are in an upward trend.

The bottom line is that the “opportunity cost” argument is “fake news” on the economics front for bank lending. Opportunity cost works in a very limited and routinely reversible way under a corridor system – due to the rapidity of money market adjustment to target changes – and due to its essential irrelevance in core lending behavior where it is capital rather than reserves is the constraining economic resource, thereby overruling the relevance of fat reserves delivered to a competitive but capital driven banking system.

JKH, I have heard, and replied to, all of the claims you make on several occasions, so I won't rehearse those replies here. I refer you and those who share your perspective to my July 2017 Congressional testimony: https://financialservices.house.gov/uploadedfiles/hhrg-115-ba19-wstate-gselgin-20170720.pdf In particular, your suggestion that banks cannot or will not typically dispose of sufficiently large volumes of excess reserves by multiplying deposits at least proportionately is contradicted by every historical episode of hyperinflation. The notion that banks won't normally hold excess reserves so long as those yield less than alternative assets remains as valid as ever. Other factors besides scarce reserves can, of course, also constrain bank lending. But the empirical evidence that banks generally lend to the full extent their reserve holdings permit is overwhelming.

DeleteIt is, of course, trivially true that if, under a corridor system, a CB manages reserves so as to never confront banks with a persistent aggregate excess supply, there need be no "hot potato" effect, or consequent nominal growth in loans, deposits, and (cet. par.) prices. But that is far from being the most common, let alone the only, possibility.

Delete"What is typically not appreciated is that banks make their risky lending decisions based on risk assessment, required capital quantity, and required return on capital. This is what determines the required credit spread."

DeleteThis is a corridor risk, banks have to estimate the volatility of returns going forward for their loan. All business have to maintain a corridor surplus, outs-ins.

So skip the hot potato effect and just have the CB take the first estimate of volatility by estimating the volatility of ins and outs over the whole domain. The problem with keeping the the hot potato effect is that we need a debt cartel to manage the bulge.

In fact, the corridor should adjust itself if the CB just limited itself to a fixed, and small, market making risk to balance loans and deposist. No policy rate, let the market determine that.

I have the biggest problem of all in understanding this:

ReplyDeleteHow did we get from competitive supply and demand to monopoly central banking?

When I look back to understand this I get the underpants theory:

1) Chapter one, econ 101, competivie supply and demand including free entry and exit

2) Paul Samuelson makes an assumption that all money is monopoly

3) Chapter two, central banking can plan, competitive market gone./

Paul Samuelson was dead wrong. Competitive currencies take up about 20-30% of the economy at any given time. Hence, any central bank is absolutely clueless about risk going forward, and has no way to set policy, except its own currency risk. 9% of the Canadian economy is US tourist dollars, another big percentage is tied to the petro dollar. The BOC is clueless, it should just keep its market making risk minimized and let the member banks set rates going forward.

There is no need to issue public debt

ReplyDeletehttp://bilbo.economicoutlook.net/blog/?p=31715

"Most of the arguments made in favour of sustaining public debt issuance can be reduced to special pleading by an industry sector for public assistance in the form of risk-free government bonds for investors as well as opportunities for trading profits, commissions, management fees, and consulting service and research fees.

***

On balance, public debt markets appear to serve minor functions at best and the interest rate support can be achieved simply via the central bank maintaining current support rate policy without negative financial consequences.

The public debt markets add less value to national prosperity than their opportunity costs. A proper cost-benefit analysis would conclude that the market should be terminated."

George

ReplyDeleteLooks like an excellent paper (your July 2017 testimony) as a representation of your views. Certainly worth reading in its entirety, and in some detail. I must say that the first 20 pages I’ve looked at so far only galvanizes the vast difference between your analysis and my own interpretation of things. But it is good writing, so I shall try to spend more time on it.

My own views come from actual experience in the function, not from heterodox cults. But certain elements from those sources, along with more upscale central bank writing and other notable academic work (e.g. Godley and Lavoie 2008), fit with my own experience.

If I can find the time to absorb your paper properly, I’ll drop a further comment here in a few days, regarding the paper.

Thanks JKH. I dashed that testimony off in several days, and am now reworking it. We should perhaps correspond about our different perspectives by email, so as not to impose on JP. My email is gselgin@cato.org

Deletethanks George

DeleteHope you don't take too much offense to my slightly blistering missive of 8:10 above, which I submitted just before seeing this

Sometimes I drop thoughts that are compressed due to my own time constraints - and there were a couple of ideas there that I thought were relevant to emphasize in terms of watching the dialogue between JP and yourself

I don't offend all that easily, JKH. I've even been known to dish it our myself every now and then!

DeleteIf JP does not mind, could you please keep the debate going here George and JKH? I am currently reading the pdf, interesting reading. My views are close to JKH/JP on this but I would rather see the debate on this paper carried on here, rather than second guess JKH's questions and criticisms (and I will stay silent in the peanut gallery).

ReplyDeleteMartin, I wish I could drag them back, but that's out of my control. Maybe they'll come back of their own accord. Glad you are enjoying the debate, though.

Delete