|

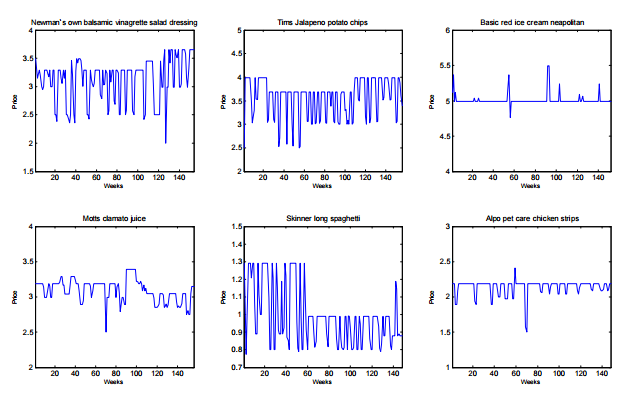

| Sticky prices illustrated, from Eichenbaum, Jaimovich, and Rebelo (link) |

What makes ride sharing firm Uber interesting is not just its use of new technology to mobilize unused car space, but the method it uses to price its services. Uber's

surge pricing algorithm varies cab fares dynamically. To get from A to B, the car that you hired this morning for $10 could end up costing $100 this afternoon.

How unlike the traditional taxi fare it is displacing! In their 2004 paper on sticky prices, economists

Bils and Klenow found that taxi fares tended to remain at the same level for 19.7 months before being adjusted. Getting from A to B pretty much costs you the same price day-in-day-out for almost two years.

In our internet age, are prices getting less sticky?

At first glance no.

Alberto Cavallo, who along with

Roberto Rigobon created

the Billion Prices Index (the bane of all

inflationistas), has

analyzed scraped data from the websites of retailers who continue to sell mostly through bricks & mortar stores, say like Walmart. Cavallo finds that U.S. online prices stay fixed for 42 days, about the same as offline prices.

On the other hand,

Gorodnichenko,

Sheremiro, and

Talavera find that online prices

exhibit more flexibility than offline prices. Unlike Cavallo, the authors analyze data from an online-only store, say like an Amazon (they aren't permitted to disclose which store). However, while Gorodnichenko et al find that online prices are less rigid than bricks & mortar prices, they still exhibit unusually long

price spells, or periods of fixity. These spells tend to endure for about 7 to 20 weeks, two-thirds shorter than offline spells when the effect of discounts/sales has been removed. The result is counter-intuitive, say the authors, given that online stores have the technology to cheaply adjust prices as supply and demand change, yet for some reason choose not to.

Even though both papers were published in 2015, Cavallo and Gorodnichenko are using relatively stale data. The first dataset runs between October 2007 and August 2010 while the latter spans the period between May 2010 and February 2012. This delay is unfortunate as the online world is changing fast. Recent industry articles point to a large ramp-up in the use of

dynamic pricing by retailers over the last few years. For instance, Profitero, a price intelligence provider, charts out a

step-wise change in the pace of Amazon's price changes beginning in late 2012. According to competing price intelligence company 360pi, by 2014 some

18% of Amazon's prices were changing daily.

The same goes for an old dinosaur like Sears. While Sears' online prices rarely underwent changes in the earlier part of this decade, around 18% of its prices are now being adjusted each day, on par with Amazon. And now Sears is trying out

digital signs in its bricks & mortar stores to ensure quicker offline price changes.

The moral economy

If we are indeed entering an Uber-style flex-price world, what underlying factors had to change for this to happen? It's not technology—we've always had the means to set rapidly changing prices, just look at financial markets. If anything had to bend in order for pricing patterns to change, it was the ethics of price setting.

To understand why, we need to explore one of the enduring questions in economics: why goods & services prices remain fixed in the face of continuously changing demand and supply conditions. When economist

Alan Blinder polled businesses in the early 1990s to find out why they kept prices unchanged for long periods of time, the most common answer was the desire to avoid "antagonizing" customers or "causing them difficulties." Blinder's findings evoked

Arthur Okun's earlier (1981) explanation for sticky prices whereby business owners maintain an implicit contract, or invisible handshake, with customers. If buyers view a price increase as being unfair, they might take revenge on the retailer by looking for alternatives. A retailer who promises to adjust prices rarely and only when costs justify it thereby avoids antagonizing customer sensibilities, and in return the customer provides a degree of loyalty.

The idea that prices are set within an overall moral framework predates Blinder and Okun. Nobel Prize winning economist

John Hicks, for instance, once wrote that the notion that all prices are perfectly flexible was highly unrealistic and attributed rigidity to legislative control, monopolistic action "of the sleepy sort which does not strain after every gnat of profit, but prefers a quiet life," and "lingering notions of a ‘just price’."

Hicks' use of the word 'lingering' refers to the extended lineage of the concept of the

just price. The belief that it is in some way sinful to sell a product for more than its fair price is

a very old one, going back to early economic thinkers like

Thomas Aquinas. In the age that Aquinas inhabited the economic roles that individual were permitted to play and the prices they could set were determined by tradition and custom. Historian

E.P Thompson once

referred to this as the "moral economy." For example, medieval English farmers could not sell their corn directly from their fields but had to bring it in bulk to the local "pitching market." Speculation, or the practice of "withholding" in the anticipation of better prices, was prohibited. Once at market, no sales of corn could be made before stated times. When the bell rang, the poor had the first chance to buy, and only after could larger dealers make purchases. These various market structures were designed to ensure a just price and fair profits.

Even as these structures were slowly unwound, writes Thompson, the English populace clung to the old morality, the physical incarnation of this being food riots which swept the countryside during the 18th century. These riots weren't random attempts to pilfer. Rather, they were relatively sophisticated affairs whereby rioters would organize to

set the price of a good, in effect forcing the offending retailer to sell their wares at the level deemed just rather than at its much higher market-determined rate.

In the same way that 17th century rioters self-regulated markets by threatening to set the price for corn or bread, modern shoppers who encounter an unjust price threaten to cross the aisles towards the competition. Eager to avoid being punished by their customers' wrath, retailers implicitly promise to keep their prices fixed for long periods of time.

I find it interesting that even when we start from scratch, the notion of a just price quickly emerges. In his account of a

temporary P.O.W. camp economy in which cigarettes circulated as money,

R.A. Radford notes that:

There was a strong feeling that everything had its "just price" in cigarettes. While the assessment of the just price, which incidentally varied between camps, was impossible of explanation, this price was nevertheless pretty closely known. It can best be defined as the price usually fetched by an article in good times when cigarettes were plentiful. The "just price" changed slowly; it was unaffected by short-term variations in supply, and while opinion might be resigned to departures from the "just price," a strong feeling of resentment persisted. A more satisfactory definition of the "just price" is impossible. Everyone knew what it was, though no one could explain why it should be so.

Behavioral economists also find evidence of a just price mentality. Using telephone surveys,

Kahneman,

Knetsch, and

Thaler were able to isolate

community standards of price fairness. Generally, consumers feel they are entitled to their

reference price, or past price. They also believe firms are entitled to their

reference profit and deem it fair for a firm to raise prices to protect that profit, say because the firm's costs have increased. A firm that takes advantage of an increase in demand by raising its price and makes more than its reference profit is, however, breaking the rules of the game and acting unfairly.

----

So let's bring this back to Uber surge pricing and Amazon/Sears dynamic pricing.

I see two angles here. After centuries of a just price morality, perhaps we are inching towards an alternative framework. Maybe we've finally overcome our revulsion to an 'unfair price' that varies according to fluctuations in demand. Instead of the 19.7 month price spells of yore, we're now willing to endure 19.7 minute price spells. Morality changes, after all; slavery and death penalties used to be common, abortion was prohibited. If so, Uber and Amazon's pricing policy are emblematic of this underlying morality switch.

Or maybe we haven't switched at all and are still operating under the old rules of the moral economy. If so, the new pricing technologies adopted by Amazon and Uber are destined to be met by a titanic wave of consumer revulsion. This may be already happening; Uber's surge pricing policy has attracted plenty of negative press (

here and

here). Morality is a powerful force; unless they want to be dashed to pieces, the offenders will have to relent and make their prices more sticky.